LINDIWE LIMITED

Calculations

| Date of cash flow | CU | |

| 01/01/2015 | Fair value – CU500 transaction costs | |

| 31/12/2015 | CU10,000 x 10% | 1,0001 |

| (CU10,000 x 110%)/2 | 5,5002 | |

| 31/12/2016 | CU5,000 x 10% | 5001 |

| (CU10,000 x 110%)/2 | 5,5002 |

1 – interest amounts paid in cash calculated on nominal value.

2 – redemptions at a premium of 10%.

Calculation of the fair value of the liability on initial recognition

| Cf0 | 0 |

| Cf1 | 1,000 + 5,500 = 6,500 |

| Cf2 | 500 + 5,500 = 6,000 |

| I/YR | 16,5 |

| NPV | = ? = 10,000,18 |

Calculation of “i” (the effective interest rate) as the present value changed due to the CU500 transaction costs that must now be recognised against the liability initially recognised at fair value.

| Cf0 | – (10,000,18 – CU500) = – 9,500,18 |

| Cf1 | 6,500 |

| Cf2 | 6,000 |

| IRR | = ? = 20,7315% |

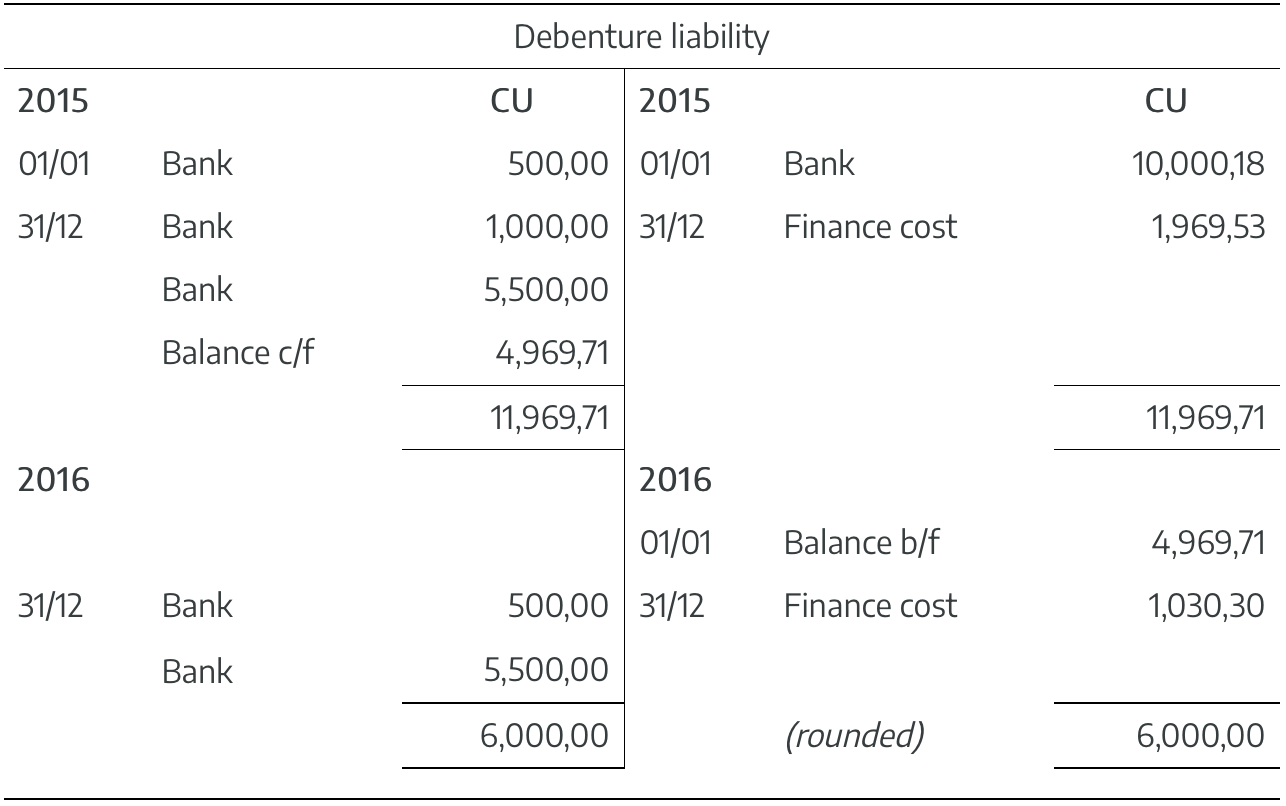

1. General journal of Lindiwe Limited

|

DR CU |

CR CU |

||

| 2015 | |||

| 01/01 | Bank (SFP) | 10,000,18 | |

| Debenture liability (SFP) | 10,000,18 | ||

| Debenture liability (SFP) | 500,00 | ||

| Bank (SFP) | 500,00 | ||

| 31/12 | Finance cost (P or L) | 1,969,53 | |

| Debenture liability (SFP) | 1,969,53 | ||

| CU9,500,18 x 20,7315% | |||

| 31/12 | Debenture liability (SFP) | 1,000,00 | |

| Bank (SFP) | 1,000,00 | ||

| Balance on Debenture liability account:CU9,500,18 + CU1,969,53 – CU1,000 = CU10,469,71 | |||

| 31/12 | Debenture liability (SFP) | 5,500,00 | |

| Bank (SFP) | 5,500,00 | ||

| (CU5,000 x 110% = CU5,500) | |||

| Balance on Debenture liability account:CU10,469,71 – CU5,500 = CU4,969,71 | |||

| 20X6 | |||

| 31/12 | Finance cost (P or L) | 1,030,30 | |

| Debenture liability (SFP) | 1,030,30 | ||

| CU4,969,71 x 20,7315% | |||

| 31/12 | Debenture liability (SFP) | 500,00 | |

| Bank | 500,00 | ||

| Balance on Debenture liability account:CU4,969,71 + CU1,030,30 – CU500,00 = CU5,500,01 | |||

| 31/12 | Debenture liability (SFP) | 5,500,00 | |

| Bank (SFP) | 5,500,00 | ||

| (CU5,000 x 110% = CU5,500) | |||

| Balance on Debenture liability account:CU5,500,01 – CU5,500,00 = R0,01 (rounding) | |||

2. General ledger of Lindiwe Limited