Purchased at discount and matures at premium in instalments

LUAN LIMITED purchases a 10% CU1,000 debenture on 1 January 2011, issued by Mandla Limited, a company listed on the JSE Limited. The debenture was purchased at 95 and matures in two equal annual instalments on 31 December, commencing on 31 December 2012, at 110. Interest is payable on 31 December. The market related interest rate for similar debentures with the same terms as this debenture is 14,1417%. Transaction costs of CU75 were paid in cash in respect of the purchase of this debenture by Luan Limited.

Luan Limited’s reporting date is 31 December. The objective of Luan Limited’s business model is to hold the debenture in order to collect contractual cash flows. The contractual terms of the debenture give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. The asset was at no stage credit impaired. Ignore expected credit losses. Mandla Limited did not designate the debenture as measured at fair value through profit or loss.

REQUIRED

- Prepare the general journal entries (cash transactions included) of Luan Limited for the years 1 January 2011 to 31 December 2013 (inclusive) to account for all matters related to the above transaction.

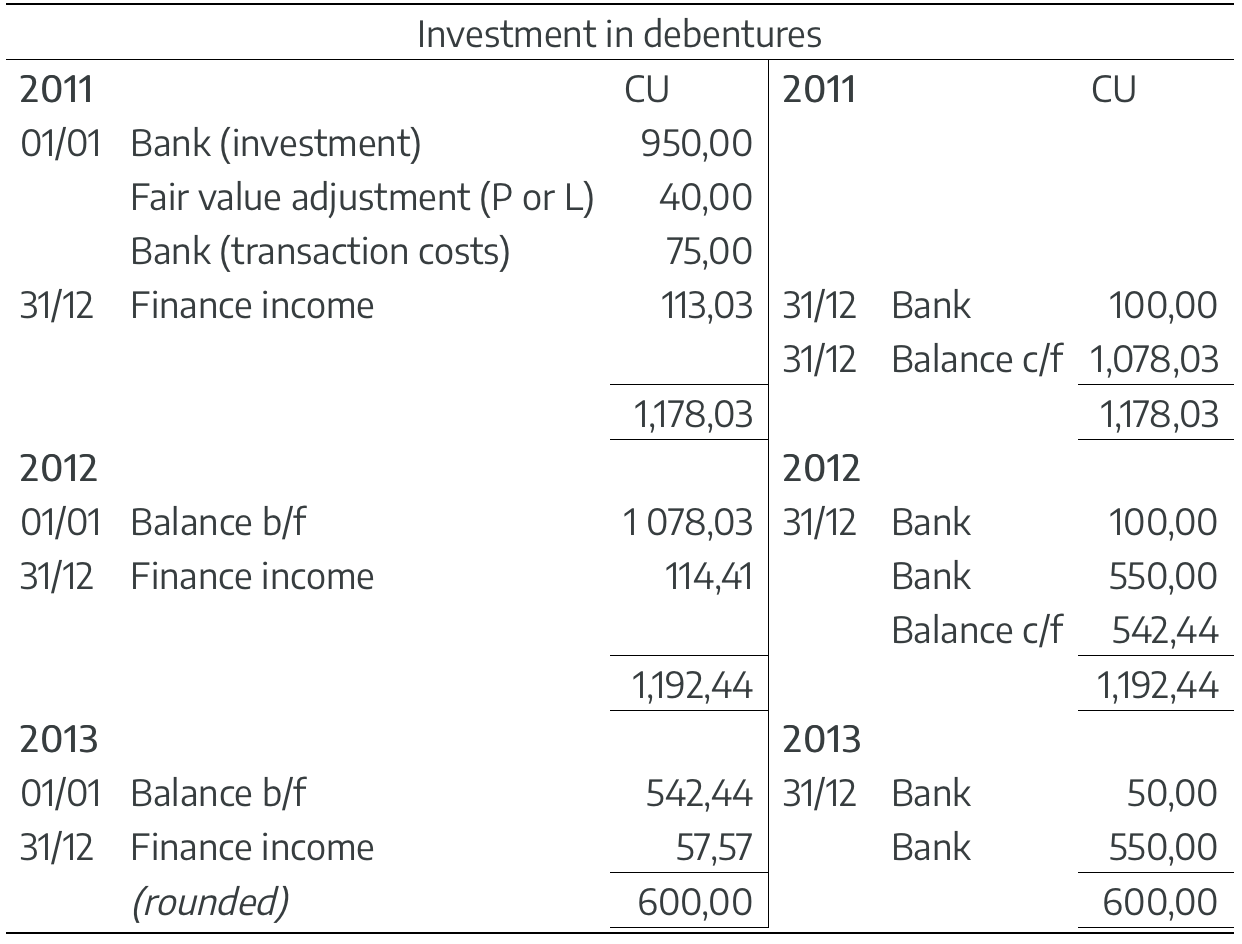

- Prepare the Investment in debentures general ledger account of Luan Limited for the years 1 January 2011 to 31 December 2013 (inclusive), properly closed off.

🇿🇦 Luan is an Afrikaans name meaning “lion” and is pronounced LU-han.

🇿🇦 Mandla is a popular Zulu name meaning “strength”. Pronounce it MAN-dhla.

SOLUTION

Calculations

|

Date of cash flow |

|

Cash flow CU |

| 01/01/2011 | (CU950 + CU75 transaction costs) | (1 025) |

| 31/12/2011 | (CU1,000 x 10%) | 100 |

| 31/12/2012 | CU1,000 x 10%) | 100 |

| (CU1,000/2) x 110% | 550 | |

| 31/12/2013 | (CU500 x 10%)% | 50 |

| (CU1,000/2) x 110% | 550 |

Calculation of the fair value of the investment on initial recognition

| Cf0 | 0 |

| Cf1 | 100 |

| Cf2 | 100 + 550 = 650 |

| Cf3 | 50 + 550 = 600 |

| I/YR | 14,1417 |

| NPV = | ? = 990 |

Calculation of “i” (the effective interest rate) as the present value changed due to the CU75 transaction costs that must now be capitalised to the amount initially recognised for the investment

The effective interest rate is defined as “the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument to the net carrying amount of the financial asset or financial liability”.

“The calculation includes all fees, transaction costs, and all other premiums or discounts.”

In this example, the net carrying amount is CU990 (fair value) + CU75 (transaction costs) = CU1,065 (rounded).

| Cf0 | -1,065 |

| Cf1 | 100 |

| Cf2 | 100 + 550 = 650 |

| Cf3 | 50 + 550 = 600 |

| I/YR | 10,6127% per annum (rounded) |

1. General Journal of Luan Limited

|

|

|

DR CU |

CR CU |

|

2011 |

|

|

|

|

01/01 |

Investment in debentures (SFP) |

990,00 |

|

|

|

Fair value adjustment (other income) (P or L) |

|

40,00 |

|

|

Bank (SFP) |

|

950,00 |

|

|

Debenture accounted for at fair value on initial recognition |

|

|

|

01/01 |

Investment in debentures (SFP) |

75,00 |

|

|

|

Bank (SFP) |

|

75,00 |

|

|

Transactions costs paid |

|

|

|

31/12 |

Investment in debentures (SFP) |

113,03 |

|

|

|

Finance income (P or L) |

|

113,03 |

|

|

CU1,065,00 x 10,6127% |

|

|

|

|

Finance income recognised at the effective interest rate |

|

|

|

31/12 |

Bank (SFP) |

100,00 |

|

|

|

Investment in debentures (SFP) |

|

100,00 |

|

|

Recognise finance income received |

|

|

|

|

Balance on Investment in debentures account: CU1,065,00 + CU113,03 – CU100,00 = CU1,078,03 |

|

|

|

2012 |

|

|

|

|

31/12 |

Investment in debentures (SFP) |

114,41 |

|

|

|

Finance income (P or L) |

|

114,41 |

|

|

CU1,078,03 x 10,6127% |

|

|

|

|

Finance income recognised at the effective interest rate |

|

|

|

31/12 |

Bank (SFP) |

100,00 |

|

|

|

Investment in debentures (SFP) |

|

100,00 |

|

|

Recognise finance income received |

|

|

|

|

Balance on Investment in debentures account: CU1,078,03 + CU114,41 – CU100,00 = CU1,092,44 |

|

|

|

31/12 |

Bank (SFP) |

550,00 |

|

|

|

Investment in debentures(SFP) |

|

550,00 |

|

|

Maturity of investment at a premium(CU1,000,00/2) x 110% = CU550,00 |

|

|

|

|

Balance on Investment in debentures account: CU1,092,44 – CU550,00 = CU542,44 |

|

|

|

2013 |

|

|

|

|

31/12 |

Investment in debentures (SFP) |

57,57 |

|

|

|

Finance income (P or L) |

|

57,57 |

|

|

CU542,44 x 10,6127% |

|

|

|

|

Finance income recognised at the effective interest rate |

|

|

|

31/12 |

Bank (SFP) |

50,00 |

|

|

|

Investment in debentures (SFP) |

|

50,00 |

|

|

Recognise finance income received |

|

|

|

|

Balance on Investment in debentures account: CU542,44 + CU57,57 –CU50,00 = CU550,01 |

|

|

|

|

Bank (SFP) |

550,00 |

|

|

|

Investment in debentures (SFP) |

|

550,00 |

|

|

Maturity of investment at premium (CU1,000,00/2) x 110% = CU550,00 |

|

|

|

|

Balance on Investment in debentures account: CU550,01 – CU550,00 = CU0,01 (rounding) |

|

|

|

|

|

|

|

2. General ledger of Luan Limited