12 Finance: 1982 Debt Crisis

| Years | Percent |

| 1970 | 0.83% |

| 1975 | 0.69% |

| 1980 | 0.77% |

| 1985 | 0.70% |

| 1990 | 0.50% |

| 1994 | 1.18% |

In August of 1982, Mexico announced that it would no longer be able to service its debt of 80 billion dollars; it was among sixteen Latin American nations to do so, alongside eleven other least developed countries (abbreviated as LDC) in other parts of the world. By the end of 1983, forty-seven individual nations were affected (Sims et al., 2020). Originating in 1970’s lending practices born from multiple global oil price shocks, real returns had decreased in rich countries, and developing countries saw their need for funds increase. This situation was tenable during the 70’s due to near-zero interest rate short term loans, but as the focus of the developed world turned to reducing inflation, and the tightening of U.S. and European monetary policy that accompanied it, this arrangement became unsustainable (Sim et al., 2020). The crisis, which arose during a global recession, further plunged the affected LDCs into economic crises as the private financing that they relied upon was abruptly cut off (Sims et al., 2020). The problem that led to the crisis was one of insolvency: the affected nations simply could not pay off their loans without major economic reforms. This observation informed the initial response of a U.S. led effort to address the crisis called the Baker Plan (Peinhardt, 2019). Private lenders were encouraged to restructure their debts, and the International Monetary Fund (abbreviated as IMF) lended the afflicted countries enough funds to cover the interest on those debts. The LDCs were given these loans on the condition that they make structural economic reforms to encourage economic growth and rid themselves of budget deficits through liberalization and fiscal austerity. This policy had several unintended consequences, leading to what is often called “the lost decade,” a period where these nations experienced a drop in per capita income of approximately 10%, high unemployment, and either non-existent or negative growth (Sims et al., 2020). Furthermore, for many nations, real wages dropped by 30% and inflation rose above 1000% (Peinhardt, 2019). This happened because many of the nations turned to reducing spending on infrastructure, health, education, and state employment. Thus, the private lenders began to negotiate loan loss provisions with their debtor nations (Sims et al., 2020). The U.S. government followed suit in 1989. Altogether, about one third of the debt was forgiven in exchange for another agreement to implement domestic reforms that would make the remaining debt serviceable known as the Brady Plan (Sims et al., 2020). The effect the crisis had on U.S. banks is reflected in the data below, showing how the net income to total capital and the net income to total assets were less than 9% and 0.5% of the industry averages (FDIC, n.d). Furthermore, between the years of 1987 and 1989, the overall income of the US banking industry fell mainly due to factors such as loan charges and loan-loss provisions (FDIC, n.d).

Besides the direct damage done to the economies and citizens of the LDCs affected by the 1982 Debt Crisis, there was also a broader problem that reverberated out of it. This being that in the rush to ensure there would not be a panic due to potential insolvency among the private lenders, regulatory standards that pertained to those banks were loosened. While this did prevent the banks from failing, it likely contributed to a weakening of market discipline and set a precedent that would encourage greater risk taking in the following decades (Sims et al., 2020). The incentivizing of economic reforms within recipient countries also became a standard part of the distribution of foreign capital in the aftermath of the Debt Crisis (Sims et al., 2020). Finally, the crisis showed the inadequacies of Import Substitution Industrialization, and led to it falling out of favor as a development strategy (Peinhardt, 2019).

Historical Background

The rising inflation in the United States reached its peak during Presidents Lyndon B. Johnson and Richard Nixon’s presidential terms. In the 1960’s, prices of everyday products rose to an all-time high, hitting consumers with the direct effects of high inflation. Government spending continued to increase as the Vietnam War stretched across decades, depleting US reserves and straining the economic strength of the nation. Nixon succeeded in securing his presidency by promising to bring an end to the conflict but was still left with a nation struggling under the consequences of inflation (Cantú et al., 2015).

The United States in the early 1970s was entering a period of stagflation, a condition in which a state is faced with high rates of unemployment as well as high rates of inflation. Choices of the past such as the gold standard and the power granted to oil producing countries caused an imbalance in the global economy. Following the tumultuous time of World War II, the “Gold Standard” gave power to the U.S. dollar by using the country’s abundant gold reserve to value the dollar. Over time as the reserves were depleted, the dependence on the US dollar continued to increase – but the country now lacked the backing to uphold the value. In 1970 when the “Gold Standard” was eradicated, the presence of oil embargoes in the global economy led to a shift in the economically dominant countries. The now “floating dollar” was valued based on its status in the market, but because of the previous reliance on the dollar to purchase oil in a global market, the oil exporting countries were able to provide an influx of dollars into Western Banks. States that had the means to produce oil controlled the prices, but the sudden increase in cost sent countries on a scramble to acquire the funds to be able to maintain enough oil for growing populations. The Western Banks were eager to loan out the funds received from oil-exporting countries, but this would eventually lead to a crisis of borrowers vs. lenders (Frieden, 2015).

The Volcker Shock in 1979 was a leading factor towards the downfall of developing country’s economies. Growing interest rates in response to inflation combined with a decrease in product demand leading to an extreme decline in the profitability of common commodities. Paul Volcker was exercising contractionary policies, attempting to control inflation at a negative impact to employment rates, and straining banks/reserves. Countries exporting goods to the United States suffered due to the drop in export-related earnings and the lowered values of local currency. These developing countries heavily depended on the export value not only to provide for any necessary imports, but also to maintain employment and avoid state bankruptcy. On top of these conditions, the introduction of the dollar into the market allowed the “purchasing price” of the dollar to increase, making it increasingly difficult for developing countries to purchase dollars needed to obtain oil and other imports on a global economic scale. The heightened purchasing price of the dollar together with increased interest rates made loan repayment nearly impossible. Countries that had borrowed had to produce increasing amounts of exports to match previous revenue as the demand and price for these goods decreased (Hilsenrath, 2021).

The incomplete loan payments shifted the blame to borrowers, with lenders also believing that the funds given out were not being properly allocated by the countries. On the opposing side, borrowers blamed the lenders for not properly vetting the states that money was granted to, and excessively distributing funds. Lenders had not thoroughly accounted for the risks associated with loans given, but the argument goes both ways – borrowers also had not responsibly planned to repay loans or allocate funds received. The conflict between lenders and borrowers was the centerpiece of the debt crisis, forcing global agencies such as the IMF and World Bank to contribute greatly to recuperating the economies of afflicted nations instead of the minimal part they had played over the past decade. The subsequent Baker (1985) and Brady (1989) Plans served to utilize new loans to cover previous loans and ensured that any debt issued would be paid back in full. The plans isolated the countries from each other, treating each one independently, and relied on cooperation between the IMF, national governments, and beneficiaries/creditors (Hilsenrath, 2021).

Main Theories and Their Takeaways

The period following the crisis’ emergence was dedicated to finding a solution to protect the U.S financial system and its solvency which signified the government’s need to design a set of strategies that could restructure the existing loans and set aside loss reserves. Given the magnitude of the situation, the regulatory system was unable to hinder the crisis and governments eventually realized that lending banks would no longer be able to recover the initial value of existing loans. This led to international efforts to rearrange from simply postponing debt to debt relief via the collection of funds from the World Bank and the IMF, as well as the conversion of bank loans into bonds that reduced the concentration risk on commercial banks. Such strategies developed thanks to a series of plans and tactics designed by the US government throughout the 1980s. As the issue continued to escalate, most banks- with government guidance- came up with a mutual three-step strategy that encompassed 1. keeping loans as current as possible 2. making time to rebuild capital and 3. transforming loans into improved assets.

The first of these plans to resolve the debt crisis was the Baker Plan, launched in 1985 at an IMF/World Bank meeting in Seoul, with the purpose of tackling the international debt crisis through structural reform. This plan was designed following the idea that China’s trade surplus could be helpful in alleviating debt among Third World countries, that were becoming increasingly indebted and incapable of relieving their own debt. The Baker Plan covered fifteen countries, ten of which were in Latin America. This strategy primarily consisted in avoiding bankruptcy of developing countries by establishing that the borrower countries could increase exports to a point that would be beneficial to reduce their debt burden to regular levels, and thus grow their way out of the debt crisis (Cline, 1989). Thus, the structural reform stressed three main points: 1. trade liberalization, 2. more liberal policies of direct foreign investment, and 3. an adjustment to the enterprise sector. More specifically, this strategy meant that industrial countries were set to contribute by increasing net loan disbursements of MBDs by providing $3 billion annually, equal to $9 billion over the course of three years. Consequently, countries in debt had to begin adopting market-oriented policies, in order to develop more productive economies so the IMF and World Bank could encourage commercial banks to increase loans to less developed countries (Aliquo, 1986). However, the Baker Plan failed at restoring LDCs to reliable credit status due to the plan’s inability to produce the increases to money flows initially predicted.

Eventually, the failed Baker Plan was succeeded by the Brady Plan, also known as Brady Bonds: a strategy that has been praised as the ultimate solution for the LDC debt crisis because of its comprehensive design that provided an optimal solution to the debt crisis. Initially, this plan was drawn by a recognition made by the U.S government about debtors not being able to pay their debts while restoring growth, which is why this strategy instead focused on seeking permanent reductions among principal and existing debt-servicing contracts, thus helping to open the floor for negotiations among creditor banks and nations in debt, which ultimately transitioned the efforts from debt rescheduling to debt relief. To illustrate, large funds were collected from the IMF, the World Bank, and other institutions to expedite debt reduction. By using these funds, LDC’s were able to implement debt-equity swaps, exit bonds, and buybacks: reducing their debt burdens. Furthermore, to qualify for financing privileges, LDCs first had to fix their economic policies by introducing reforms that encouraged growth and augmented their debt-servicing capability inside their domestic economies. Overall, this strategy discounted the debts by reducing interest rates and ensuring repayments. The Brady Plan eventually succeeded in reducing debt servicing by a significant amount. As a result, the Brady Plan evolved into the first step for LDCs to borrow and fix their markets again since WWII (Peinhardt., 2019).

In addition, as the crisis spread across nations in Latin America, the U.S government created a simultaneous solution known as the International Lender of Last Resort, which utilized fractional reserve banking and a government monopoly of legal tender issuance to serve as a failsafe for Latin American countries. Altogether, the International Lender of Last Resort became a source of money and liquidity guarantor with a macroeconomic responsibility of ensuring liquidity of the economy as a whole, serving to address the ‘’panic-induced collapse of the fractional reserve banking system.’’(Saxton, 1999). The International Lender of Last Resort can prevent credit problems from further devolving into monetary crises. On the other hand, solutions were also implemented with the use of regulatory forbearance, which is a central policy that allows financial institutions to continue working and providing their services, even if their capital is entirely drained by regulators extending the time periods for banks to adhere to regulatory needs. Therefore, during the 1982 crisis, forbearance was given to large banks with reserves against LDC loans, this has been noted to be necessary by some scholars given that the majority of the largest banks in the U.S were assumed to be insolvent, so instead of creating panic among the current banking system, regulators chose an easier route of requiring U.S banks to cast aside some reserves for LDC debt, showing priority for keeping the stability inside the banking system. In fact, forbearance gave the lending institutions time to come up with new preparations with their LDC debtors, while gaining extra capital that will make up for the losses among Latin American loans, making them less impactful.

After long years of negotiations and economic strategy development for LDCs, the Debt Crisis of 1982 came to an end after the world’s largest banks, recognizing the failures of the Baker Plan, developed a successful strategy for resolving the crisis through the Brady Plan.

In the Baker plan there were multiple actors involved, such as the World Bank and other developmental banks, which were all due to the help of Mr. Baker himself (Bindert, 1986). Mr. Baker called the World Bank and helped the debtor nations even more, as well as the commercial banks helping loan the fifteen indebted countries (Bindert, 1986). Ten of these Latin American countries were Argentina, Brazil, Venezuela, Uruguay, Chile, Ecuador, Colombia, Peru, Bolivia, and Mexico, which was the first debtor nation to carry out this plan (Bindert, 1986). During the debt crisis in Mexico it was hoped that the debtors would be finally out of debt since capital markets became accessible, but it actually went in the complete opposite direction (Rabobank, 2013). The economy stopped growing, inflation increased drastically, and debt went much higher (Rabobank, 2013). To be more specific, external debt went up over 50% of GDP in the late 1980s, which mainly symbolizes the failure of this plan (Rabobank, 2013). In conclusion this plan resulted in the failure of the Baker plan, but later on a new plan emerged which ultimately was successful.

Mexico: Debt Crisis and the Brady Plan

|

External debt |

% of GDP |

|

1978 |

≈35% |

|

1979 |

≈32% |

|

1980 |

≈30% |

|

1981 |

≈31% |

|

1982 |

≈50% |

External Debt Burden between 1978-1982 (Rabobank, 2013)

In February 1982, the Mexican government was forced to lower the value of the peso and increase the “dollar debt burden” (Rabobank, 2013). During mid-1982 the United States and the Federal Reserve Chairman gave out a 1.5 billion dollar loan to Mexico, with 2 billion dollars of cash as well but only under the 90-day rollover rule (Rabobank, 2013). When the Brady plan was created after the failure of the Baker plan, institutions like the IMF and the World Bank wanted to focus on decreasing debt instead of rescheduling them (FDIC, n.d). FDIC also states “It is estimated that under the Brady Plan agreements between 1989 and 1994, the forgiveness of existing debts by private lenders amounted to approximately 32% of the $191 billion in outstanding loans, or approximately $61 billion for the 18 nations that negotiated Brady Plan reductions” (FDIC,.n.d). With the Brady plan being successful in reducing down debt and helping lenders loan to the debtors, the International Lender of Last Resort also made an impact during the debt crisis. As previously mentioned, the International Lender of Last Resort was created by the United States as a cooperative partnership through institutions and banks (Sims et al., 2013).

According to Sims et al. (2013), commercial banks came to a conclusion they had to redistribute the debt of Latin American countries, and the IMF, alongside other agencies, funded the LDCs to pay their interests on their loans. In other words, the IMF and other banks were the main actors involved in the rescue commitment in order to help LDCs stabilize their economies. Hayes (2020) mentions as well that the Federal Reserve acts as “the lender of last resort to institutions that do not have any other means of borrowing, and whose failure to obtain credit would dramatically affect the economy.”

Brazil: Debt Crisis and Import Substitution Industrialization

The debt crisis in Brazil is best framed and contextualized by the Brazilian economic model of Import Substitution Industrialization (ISI). ISI began as an economic framework in the 1930s and 1940s predominantly in Latin America, and particularly in Brazil. This framework emphasizes developing domestic industry for domestic consumption rather than building industry for the sake of exporting to the foreign market (Guimarães 2010). This is done by stimulating domestic expansion via government subsidies, tax breaks, and state ownership of certain industries; in addition, imports under the ISI model are limited by tariffs and outright bans on certain goods (Guimarães 2010). All these policies are meant to develop domestic production where goods stay within an economy to stimulate domestic production and consumption, and thus wealth production.

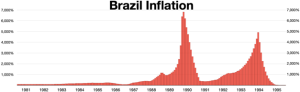

In the context of Brazil from the 1960s to 1980s, the economy flourished with an average GDP growth of 9% (Macrotrends 2023). However, the economic tides reversed by 1982 as the international debt crisis infected the Brazilian economy. ISI is a model heavily reliant on foreign investment because of its emphasis on developing capital-heavy industries, such as steel and heavy industry manufacturing. When foreign investment dried up, the Brazilian government- already heavily in debt- was unable to sustain the level of investment able to maintain a system of ISI. The economy collapsed, with inflation reaching meteoric levels.

In exchange for access to the funds of the Brady Plan, Brazil- like other Latin American nations- began a process of liberalizing its economy in the 1990s. With liberalization came an opening of the country to imports through reducing tariffs and lifting of import bans, leading to a growth in both imports and exports. Slowly, the economy began recovering, and inflation rates fell in the 1990s as a result of liberalization and the economic recovery produced by the Brady Plan.

A clear example of the effects of Brazil’s protectionist policies came from its computing industry between 1984-1992 which greatly limited the import of foreign made hardware and software. Not enough government funding was given to research which resulted in products that were of much lower quality and more expensive than those from foreign competitors. By the time this ban was lifted most of the developed countries were using computers in all their economic sectors while very few businesses in Brazil were digitizing their work still using paper methods.

The story of Brazil during the 1982 Debt Crisis is a cautionary tale regarding the limits of Import Substitution Industrialization for generating long-term economic growth. While Brazil witnessed immense economic growth in the decades prior, the lesson of 1982 is that an economy entirely reliant on foreign debt will inevitably collapse when sources of debt dry up due to global economic crisis.

Criticisms of Responses

During the years following the breakdown of the crisis, many scholars and critics studied the strategies that were used to put an end to the crisis. Therefore, some opinions that emerged are valuable to highlight here in order to understand the strategies more in-depth after reviewing how they were useful for resolving the Debt Crisis of 1982. Respectively, the Baker Plan was highly criticized because it initially aimed to administer LDCs the necessary money and policies to keep debt levels untouched and for them to be capable of managing their debt more easily; however, this theory quickly proved to be ineffective given that major banks did not increase their lending to debtor countries, and these nations also failed to commit to reorganizing their internal economies. For the Baker Plan to be successful, critics argue that the fundamental approach to get out of the debt crisis will directly have to come from fixing economic policies inside the debtor countries. The main mistake behind the Baker Plan was resolving problems for lenders, instead of resolving the issues faced by borrowers, distinguishing the plan as counterproductive because it eventually led to the exhaustion of the ability of creditors to contribute with financial assistance, making such a strategy unreliable for the crisis and for any future financial international issues (Cavallo, 2020).

As for the Brady Plan, it was constantly said to be successful after still recognizing that shareholders of the world’s largest banks had to assume losses after also taking over a decade of negotiations to make it successful. Nonetheless, it was the strategy that put an end to the issue and continues to be highlighted today given that its strategy was capable of reducing debt in a constantly growing economy, in order to regain growth that stimulates new capital sources.

Conclusion

The focal point of the Debt Crisis is highlighted by the conflict between borrowers and lenders. Borrowing entities such as developing countries, struggled under the demands of lenders needing loan repayment. The inadequate assessment of the risks of excessive lending inserted funds improperly into the global market. This left developing countries to fall into bankruptcy while lending countries suffered the consequences of inflation. A dependency on external agencies such as the IMF provided some relief to the economic strain but can not be accepted as a permanent solution.

Historically, the reliance of states on other nations or organizations to solve issues has created an imbalance in global politics. These repeated actions continue to have negative impacts on the global market, as well as the functionality of cohesiveness between state economies. After the initial solution to the Debt Crisis was formulated, similar patterns appear; the IMF is brought in to support developing countries and the cycle of dependency continues. Although the intention to build infrastructure and policies that will enhance the independent economic status of the nation persists, corruption and self-interest derail the efficacy of outside involvement (Hilsenrath, 2021).

The Brady and Baker plans were arguably inherently flawed in their continuation of the dependence created by renewed loans. Countries were given new loans to pay off existing ones but the original issue still wasn’t addressed; these nations still lacked the structure to utilize funds efficiently and not enough work was being done to build a stronger economic foundation. The fixation on the monetary part of the crisis allowed ignorance of weak economic systems, further increasing possibilities of the pattern to repeat in the future (Frieden, 2015).

From a logical perspective, the borrower vs. lender conflict could be avoided if loan distribution was based on country prosperity and if countries borrowed based on ability of repayment. In a real world standpoint, the loss of exports from less financially stable countries and the abundance of funds in reserves led to price increases, inflation, and unemployment. The difficulty of choosing between the two results leads to the construction of multiple, short-lived policies that can allow the global economy to retain some balance and continue providing benefits to participating nations. When other factors such as war, embargoes, political tension, and resource depletion are considered, the probability of finding a solution with longevity narrows (Frieden, 2015).

Works Cited

Aliquo, N. A. (1985). Treasury Secretary James Baker’s Program for Sustained Growth for the International Debt Crisis: Three Steps toward Global Financial Security. Dick. J. Int’l L., 4, 275.

Bogdanowicz-Bindert, C. A. (1986). The Debt Crisis: The Baker Plan Revisited. Journal of Interamerican Studies and World Affairs, 28(3), 33–45. https://doi.org/10.2307/165706.

Cantú, C., Park, K., & Tornell, A. (2015). Lessons from the 1982 Mexican Debt Crisis for Greece. VoxEU.org. https://voxeu.org/article/lessons-1982-mexican-debt-crisis-greece.

Monteagudo, M. (n.d.). The debt problem: The baker plan and the Brady Initiative: A Latin American Perspective – core.ac.uk. Retrieved April 20, 2022, from

https://core.ac.uk/download/pdf/216911883.pdf.

Cavallo, E. (2020). Baker or Brady: Lessons of past financial crises for the pandemic recovery. Ideas Matter. Retrieved April 21, 2022, from https://blogs.iadb.org/ideas-matter/en/baker or-brady-lessons-of-past-financial-crises-for-the-pan demic-recovery/.

Fincyclopedia. (2020). Regulatory forbearance. Fincyclopedia. Retrieved April 21, 2022, from https://fincyclopedia.net/banking/r/regulatory-forbearance.

Frieden, J. (2015). Latin American Debt Crisis of the 1980s (Jeffry Frieden, Harvard University). Www.youtube.com. https://www.youtube.com/watch?v=zhV9x79PLRU&ab_channel=AddingtonCoppin

Guimarães, A. Q. (2010). State Capacity and Economic Development: The Advances and Limits of Import Substitution Industrialization in Brazil. Luso-Brazilian Review, 47(2), 49–73. http://www.jstor.org/stable/40985095

Investopedia. (2021). Investopedia. Retrieved April 20, 2022, from

https://www.investopedia.com/terms/l/lenderoflastresort.asp.

Jilsenrath, Jon (2021). What the Inflation of the 1970s Can Teach Us Today | WSJ. Www.youtube.com.

MacroTrends (n.d.). Brazil GDP growth rate 1961-2023. Retrieved April 18, 2023, from https://www.macrotrends.net/countries/BRA/brazil/gdp-growth-rate

Peinhardt, C. (2019) Finance and Development 1 [Lecture]. University of Texas at Dallas, Richardson, TX, United States.

Rabobank (2013). The Mexican 1982 debt crisis. Rabobank. (2013, 19 September).

https://economics.rabobank.com/publications/2013/september/the-mexican-1982-debt-crisis/#.

Saxton, J. (1999). An lender of last resort, the IMF, and the Federal Reserve. Retrieved April 22, 2022, from https://www.jec.senate.gov/public/_cache/files/9d33ca4c-2518-49e3-abee 332698e16597/unemp loan-international-lender-of-last-resort-the-imf-and-the-federal-reserve—feb 1999.pdf

Sims, Jocelyn, and Jessie Romero. (2020). Latin American Debt Crisis of the 1980s. Federal Reserve History. https://www.federalreservehistory.org/essays/latin-american-debt-crisis. – The LDC Debt Crisis. (n.d.). In History of the 80s (Vol. 1 – An Examination of the Banking

Crises of the 1980s and Early 1990s) (Vol. 1, p. 20). FDIC.

https://www.fdic.gov/bank/historical/history/191_210.pdf.

Wikideas. (n.d.). File:Brazil inflation 1981-1995.WEBP. Wikimedia Commons. Retrieved April 18, 2023, from https://commons.wikimedia.org/wiki/File:Brazil_Inflation_1981-1995.webp

Wikimedia Foundation. (2021). Baker Plan (debt relief). Wikipedia. Retrieved April 21, 2022, from https://en.wikipedia.org/wiki/Baker_Plan_(debt_relief).