11.4 The Derivation of Annuity Factors (Solution)

Below you will find the solution to the problem on the prior page. Note that if you had an interest rate table for annuities, you would be able to multiply the annuity cash flow (in this case, $100) by the appropriate factor. You would then arrive at the future- or present-values of the cash flows, in one step. Such annuity interest tables exist; a link is provided at the bottom of this page.

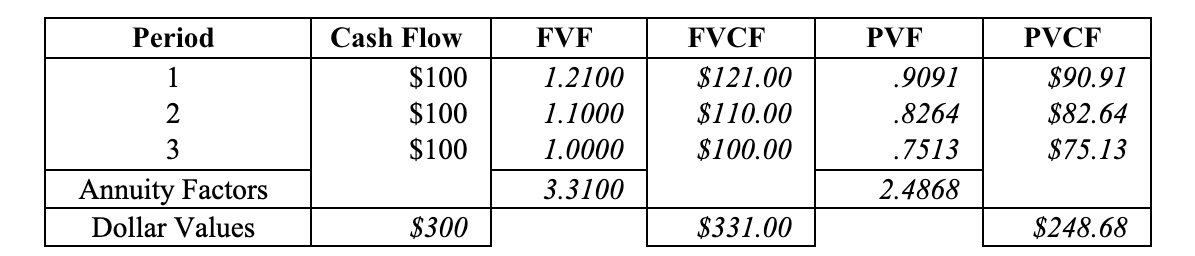

What may we observe from this table? Future value annuity factors are always greater than the number of periods. Here the FVF was 3.31, or greater than n · p = 3 periods. This is because the annuity multiplier is the sum of each respective yearly factor, each of which is greater than 1.0 (except the last one, which = 1.0) since they are all multiples of (1 + R) n. (This assumes that R > 0.)

Contrarily, each PVF is less than the number of periods because the respective factors are all less than 1.0, as each factor is the reciprocal of (1 + R) n. (Again, this assumes that R > 0.)

When utilizing a table, it is always a good idea to “eyeball” the factors you are using to make sure you didn’t lift the figure from the wrong table or make some other error. Use your head at all times. Do not be a robot!

The present value of the annuity is $248.68. If you, alternatively, had had a single sum in the amount of $248.68, and had invested it for three years at 10%, you would have $331 at the horizon:

($248.68) (1.10)3 = $331

and

$331 ÷ (1.10)3 = $248.68

Here are some more simple- and annuity- interest rate tables for you to use: